Aggregating open markets

From NFT marketplaces to infrastructures

With traditional digital assets, the power to determine access and use rests solely with the central authority. Take the case of Google's decision to shut down Google Domains and transfer all its 10M+ domains to Squarespace. If you bought a domain on Google Domains, it was automatically transferred to Squarespace, and you might need to pay double going forward to renew your domain.

Another more recent instance is Elon Musk's seizure of multiple handles (with half a million followers) without any monetary compensation.

In Web2 ecosystems, platforms like Amazon and Uber function as intermediaries, managing both supply and demand. They exert considerable control over the user experience, data, and, ultimately, the transaction itself. The power of centralization allows them to direct consumer demand towards certain suppliers, thereby securing a firm grip on their respective markets. A prime example is Amazon's push for private-label goods that mirror popular items, encroaching on existing suppliers' market share.

NFT marketplaces, in contrast, disintermediate assets; there is no necessity for an intermediary who can monopolize demand, making these platforms a perpetual battleground with no durable supply moats. Users maintain full control of their NFTs within their digital wallets, granting them the freedom to explore multiple platforms to find and directly transact with counterparties through secure, instantaneous exchanges. By utilizing ENS, the web3 version of internet domains, individuals can establish a unique digital identity that is unseizable and also universally recognized across various social media platforms.

NFTs are blockchain-anchored assets that manifest digital scarcity. The blockchain records every NFT's origin, ownership, and transaction history in a transparent and unalterable manner. As a result, NFTs are not tethered to any single platform or marketplace; they can be purchased, sold, exchanged, and owned by anyone, anywhere in the world.

In this new paradigm, building defensible moats becomes a Herculean task for NFT marketplaces. Traditional growth strategies that solved the "cold start" problem are less effective, as users are free to gravitate towards the "hot" platform with more juicy incentives.

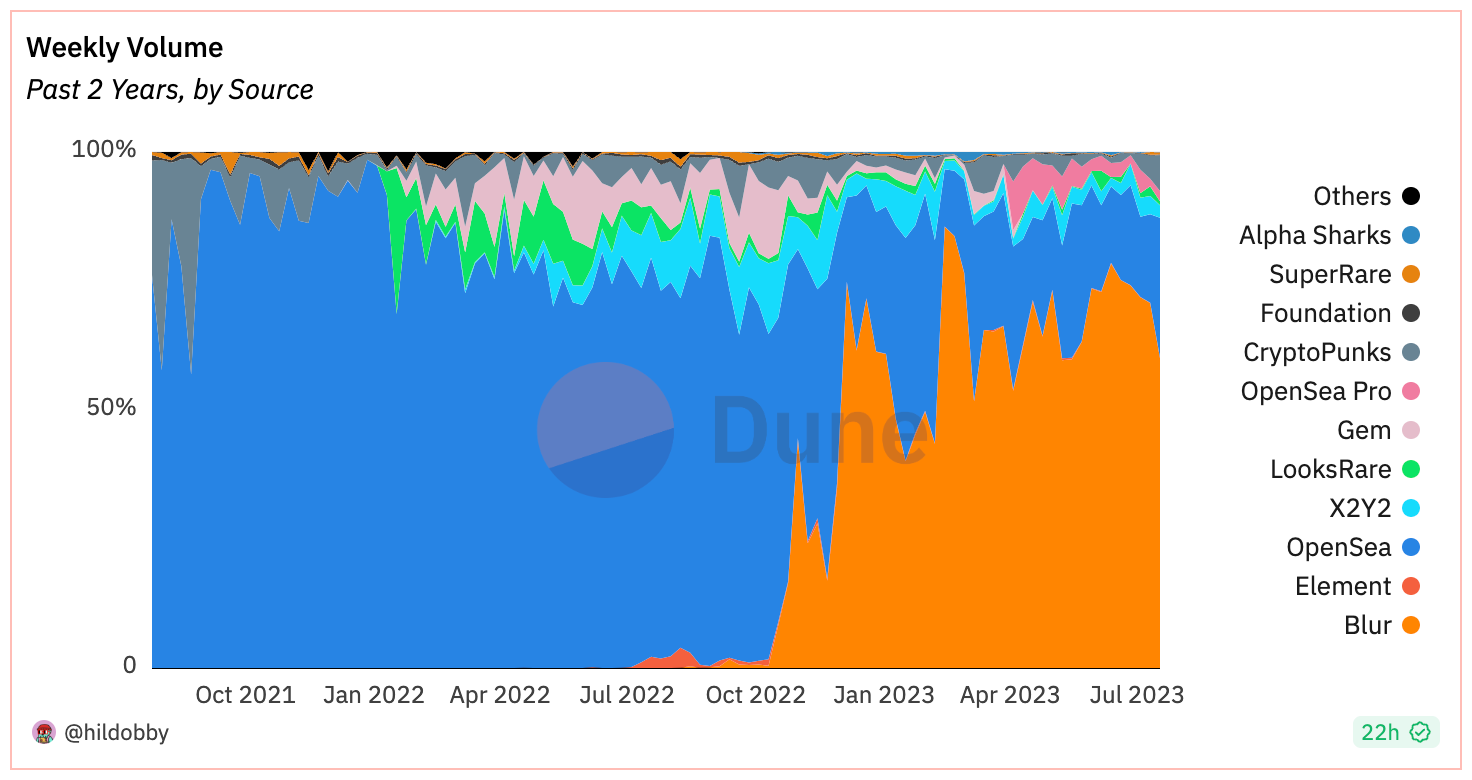

In this context, the rise of OpenSea as the victor of the NFT bull market, warding off contenders like Looksrare and X2Y2, offers a fascinating case study. Interestingly, a new challenger named Blur emerged in the latter half of last year, successfully chipping away at OpenSea's market share.

In this piece, we'll dig into Blur's strategy for controlling liquidity, and the broader developments shaping NFT markets.

Opensea’s Horizontal Play

Joel John’s examination of Aggregation theory looks at how web3 offers some distinct advantages for marketplaces- with the decreasing costs of verification and scaling, marketplaces can easily add support for new projects and integrate with various blockchains.

OpenSea (OS) capitalized on its first mover advantage of being the first NFT marketplace on Ethereum, swiftly expanding into multiple chains - Solana, Polygon, Arbitrum, and Optimism, becoming a one-stop destination for NFT collectors.

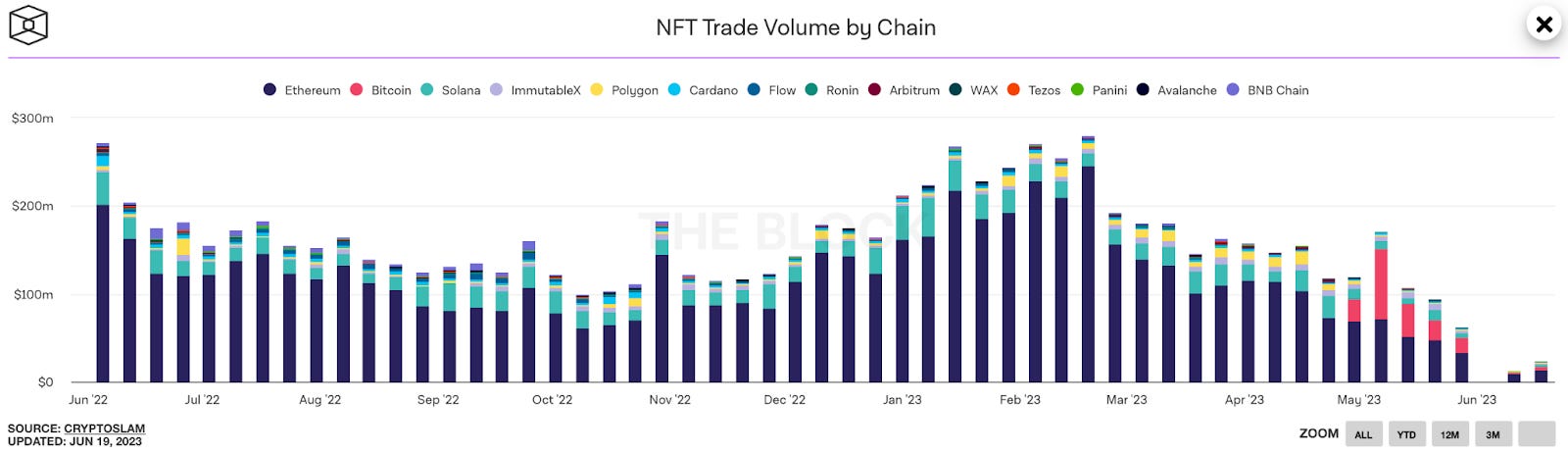

While Ethereum birthed NFTs with adorable Cryptokitties and pixelated Cryptopunks, other chains have seen comparatively slower success. In February 2023, when Blur's airdrop and Yuga Labs’ Dookey Dash game juiced the markets with fresh liquidity, Ethereum's weekly volumes stood at $200 million. Following Ethereum were Solana at $25 million, Polygon at $10 million, Immutable at $5 million, and a combined $5 million split among Arbitrum, Flow, BNB, and others.

OS set the gold standard for NFT commerce, presenting users with a reliable, cost-effective, and secure trading platform. In spite of several customer complaints and sluggish product improvements, OpenSea grew into a $13 billion juggernaut within two years, earning over $1 billion from a 2.5% cut from every transaction.

Other NFT marketplaces such as Looksrare and X2Y2 eyed this success and tried to take advantage of OS’s user base. They provided a one-time token distribution to users in the form of an airdrop. Instead of the transaction fees benefiting the team, they shared trading fees with buyers and sellers depending on how much they traded. These incentives led to a spike in trading activity, but as the token incentives waned, these platforms grappled to retain and foster a dedicated user base.

To navigate this fragmented landscape, aggregators surfaced as an elegant solution, consolidating NFT bids from multiple platforms into a singular, streamlined dashboard. Gem and Genie emerged as frontrunners, attracting traders with enhanced features like gas-optimized multi-buys(sweeps), trait-centric purchasing, and cross-platform sales capabilities.

Recognizing the aggregators' influence, OpenSea strategically acquired Gem, rebranding it as OS Pro, its offering for ‘‘pro collectors’’. Not one to be sidelined, Uniswap also expanded its portfolio by acquiring Genie, enhancing its view beyond just ERC20 tokens.

Blur’s Vertical Play

Blur debuted in October 2022, targeting the high-stakes arena of professional traders, who require high liquidity and cheap transaction costs. With sophisticated trading tools, zero marketplace fees, optional royalties, real-time data updates, and analytics tailor-made for traders, Blur's entry was a game changer.

Blur positioned itself as a marketplace + aggregator - By funneling bids from other marketplaces, Blur presented one cohesive experience to traders. If a user put an NFT up for sale on OS, Blur would detect this through OS APIs and list it on Blur ensuring that users always had access to the best selection of NFTs across Blur and other platforms such as OS, LR, X2Y2, Sudoswap, etc.

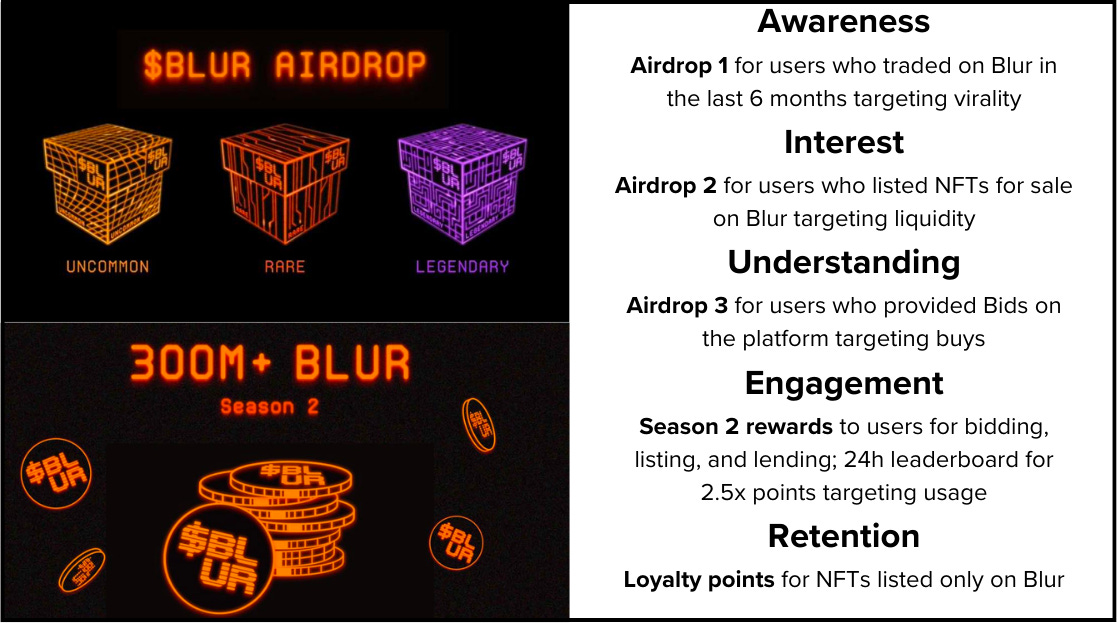

One of the standout aspects of Blur's launch was a phased airdrop strategy, luring traders from other platforms with generous rewards. By trading through Blur, not only could users tap into OS's NFTs without any fees (compared to the usual 2.5%), but they also stood to gain from Blur's airdrops.

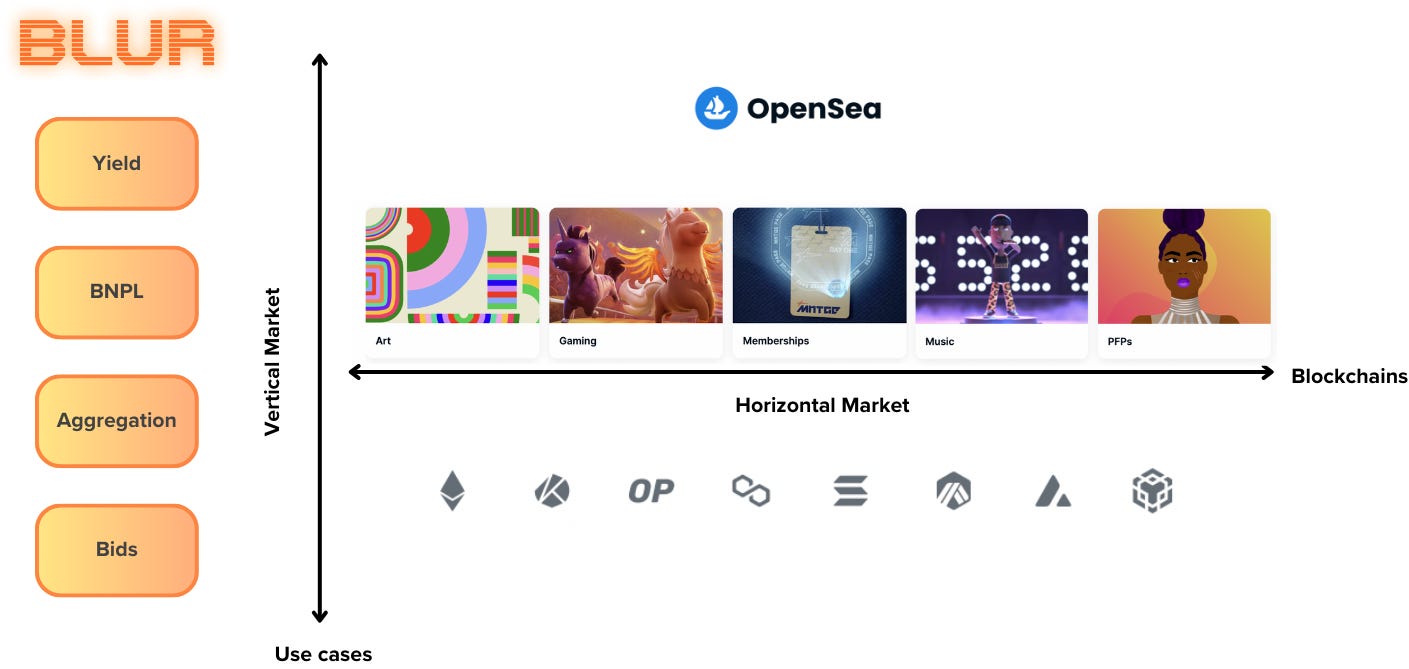

While OpenSea, focused on aggregating NFT purchases for the average user, Blur had a different vision. It aimed at aggregating diverse use cases specifically designed for the professional trader. Instead of adding multiple blockchains, it focused on Ethereum and drove higher liquidity for the top collections.

Expanding vertically, it started offering loans with NFTs as collateral and introduced a "Buy Now, Pay Later" option for buying NFTs on leverage. This was more than a marketplace; it was a holistic ecosystem for professional trading.

Fast forward to today, Blur commands an impressive 70% market share on Ethereum NFT volumes, having surpassed OpenSea in just half a year. Let’s dig into their strategy and how they managed to grow so quickly:

- Royalty-free Transactions - A true magnet for traders looking to conduct high-frequency NFT transactions. This move spurred a flurry of complaints from creators during the 'royalty wars', leading to demands for mandatory NFT royalties. For now, Blur enforces a minimum royalty of 0.5%.

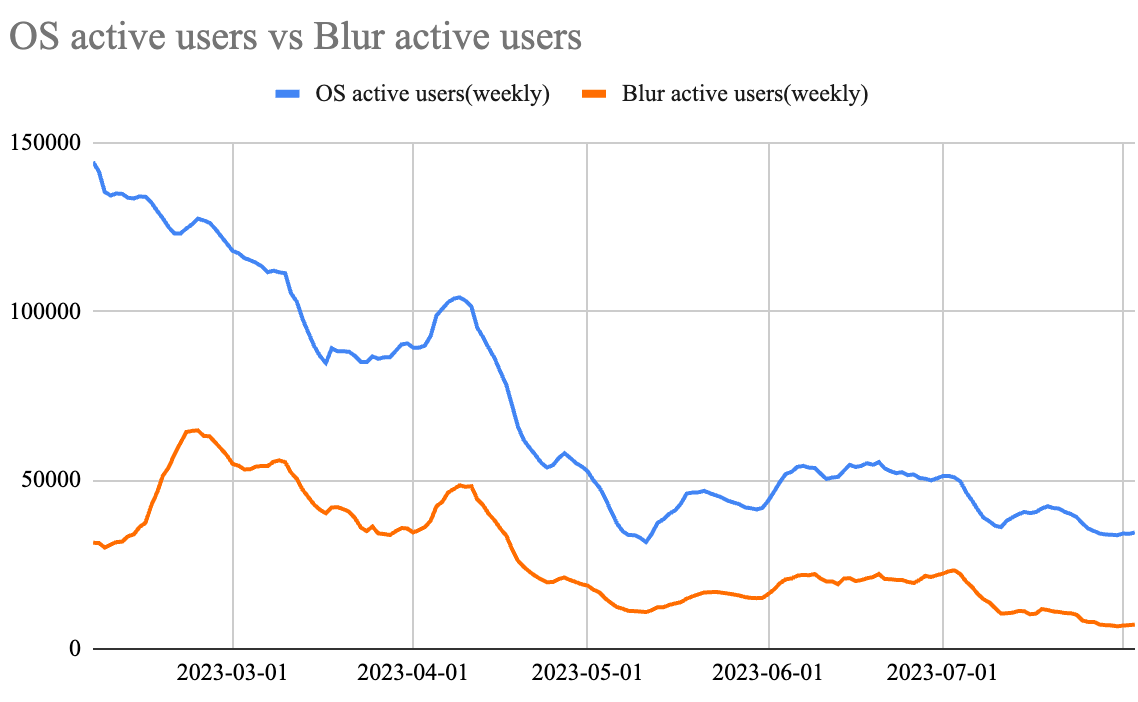

- Pro Trading Experience- Focus is not on collecting the most artistic NFT but on sweeping and trading. Though Blur attracts fewer traders at 30% of weekly traders, they contribute to ~70% of NFT volume.

- Targeted airdrops - Blur targeted rewards against their own product goals - by encouraging users to bid and sell on their platform to earn rewards, they created a loyal base of users who understood the platform and loved using it.

Blur also gamified these drops - users get care packages and the amount of BLUR inside has a random component making it difficult for users to calculate EV of airdrops and farm rewards. While there is a significant amount of wash trading on Blur to exploit rewards, data indicates that this is close to 14%, which is on the lower end compared to other marketplaces where farming is straightforward.

- Liquidity Management- Blur launched a Bidding pool for users who wanted to earn airdrops for providing NFT liquidity. This is a contract-controlled pool, where users have to deposit Ether in Blur’s pool and can withdraw anytime without Blur’s approval. Users can use funds in the pool to set bids and earn airdrop rewards. This not only enhanced the bidding experience and user satisfaction but also secured a competitive edge by retaining liquidity. Once users allocate their Ether to Blur's pool, they tend to stay loyal, leveraging Blur's array of NFT services without incurring gas fees.

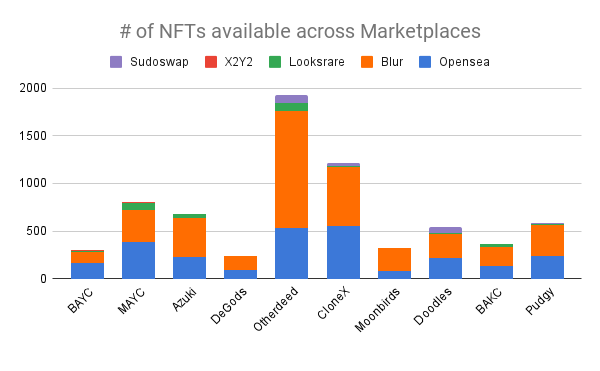

- Market Depth-By incentivizing close-to-floor-price bids, Blur managed to provide a higher floor depth to NFTs, absorbing massive dumps and showing remarkable liquidity control. For buys as well, Blur has more NFTs listed, probably to earn reward points for listing.

- Lending Services- Blur decreased the capital barrier to access blue chip NFTs by offering loans with their new product - Blend. Almost 50% of Blur's trading volume comes from lending. Lending also freed up capital for NFT whales as they could lock NFTs as collateral and borrow dollars.

Now that we looked at how these marketplaces are faring, let’s turn our attention to the industry as a whole.

Mapping the transition from Marketplace to Protocol

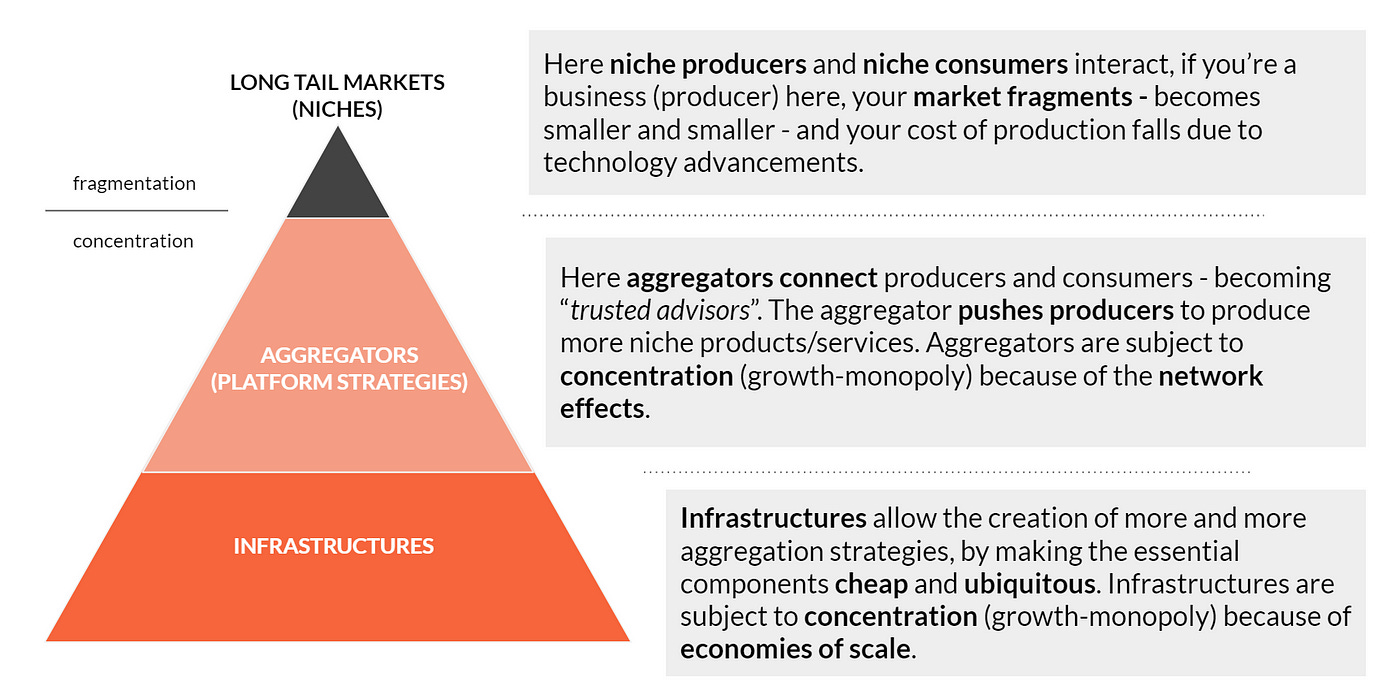

Boundaryless, the consulting firm renowned for its research on platform ecosystems, suggests that platforms transition into a three-layered structure. They've termed this concept "Cicero's Triangle" after the founder, Simone Cicero.

This model, with its three-layered structure: 'Long Tails', 'Aggregators', and 'Infrastructures', sketches out the anatomy of web2 platform markets. To summarize it simply - Think of it like a three-layer cake, where each layer brings its unique flavor but they all work together to create a delicious whole.

Platforms, in their initial phase, often start as marketplaces serving the long tail of demand. They provide a space where buyers and sellers can meet and transact. This is the first step in creating a network effect, where the value of the platform increases as more users join. Amazon started by selling books to tap into the long-tail demand.

"Books were great as the first best because books are incredibly unusual in one respect, that is that there are more items in the book category than there are items in any other category by far.”- Jeff Bezos

Long Tails denote the substantial number of independent entities that produce products or services independently. Individually, these players may not achieve widespread popularity or profitability, but collectively they contribute significantly to the overall market. An Airbnb host or a seller on Amazon embodies this role.

Over time, successful platforms evolve into aggregators. They do more than just facilitate transactions; they start to control the user experience. They aggregate the supply side of the market (the sellers or service providers) and present it in a way that is easy for the demand side (the buyers or users) to consume.

This is where platforms start to exert more control and capture more value. They standardize transactions, manage reputations, and provide tools and services that make it easier for the supply side to serve the demand side. This aggregation creates even stronger network effects and makes the platform more valuable to all users. Airbnb is an example of an aggregator in Web 2.0, consolidating property listings from global hosts and connecting them with potential guests.

Finally, as platforms mature, they move into the infrastructure layer. They become so integral to the functioning of the market that they are essentially the market's operating system. They provide the foundational technologies and services that enable the entire ecosystem to function. At this stage, platforms have the potential to capture even more value, as they are deeply embedded in the operations of the market.

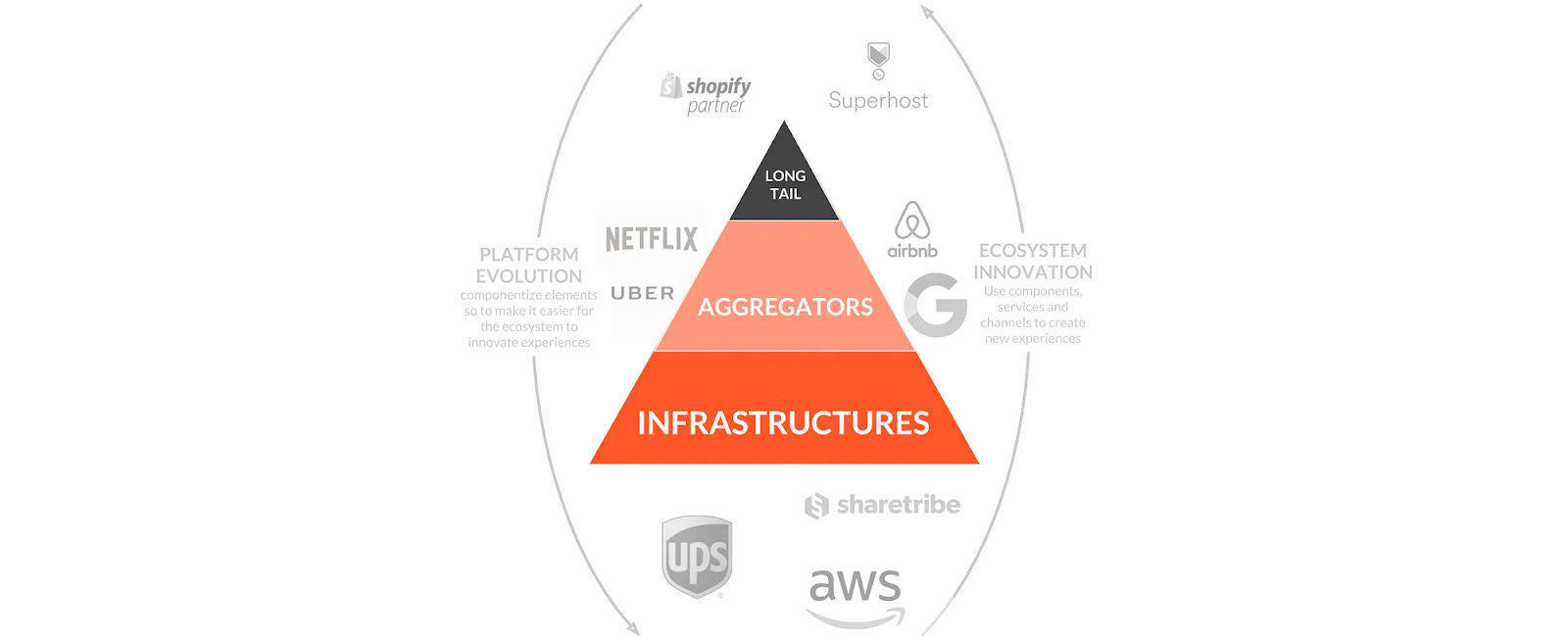

The internet’s evolution mirrors this progress. Initially, firms hosted websites on their own servers in their basement. As the internet expanded and demand for computation increased, shared hosting took off where websites could tap into a common pool of server resources.

AWS converted cloud hosting into infrastructure as a service, making it extremely easy for users to buy scalable cloud storage on demand moving demand downwards from self-service to a standardized pay-as-you-go model.

Boundaryless highlights how such standardization spawns new use cases and offerings. AWS catalyzed collaborative practices like Agile and DevOps, enhancing collaboration and efficiency. This paved the way for low-latency experiences powering platforms like Spotify and Netflix that focused on new niches and delivered delightful experiences.

As E-commerce on the internet grew, sellers servicing the long tail could create their own online stores and interact directly with customers. The democratization of commerce led to an impressive 10% of the global E-commerce market transacting through Shopify-built stores ($200 Bn GMV in 2022).

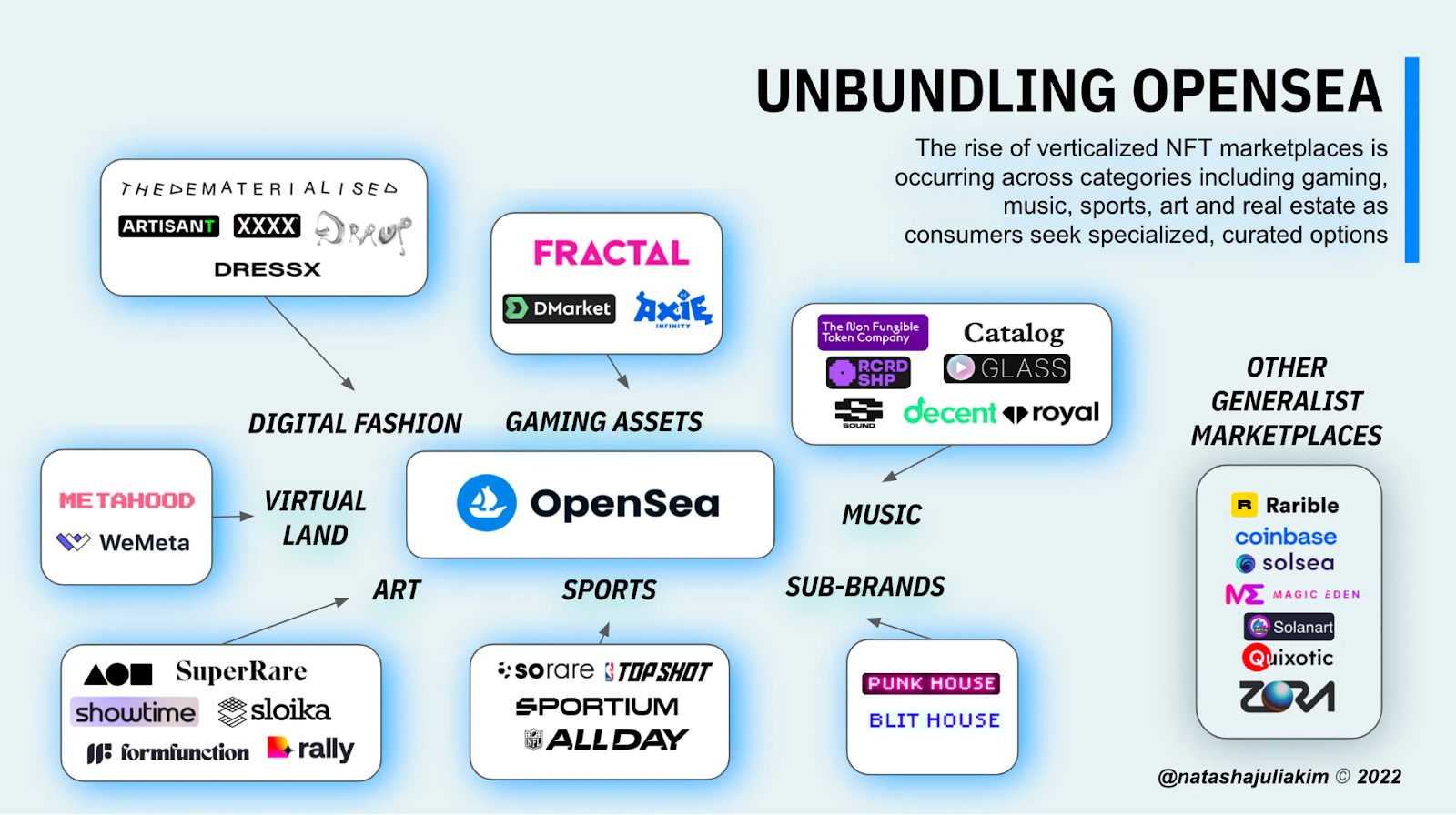

We foresee that NFT marketplaces’ are also going through this evolution, starting from the long tail and moving towards an infrastructure layer that can power the next generation of NFT apps.

Long Tails: The Niche Markets

NFTs allow niche creators to thrive by transforming fans into stakeholders. This "Long Tail" phase is more than a business model; it's a cultural shift that provides monetization opportunities to 25M+ creators.

Users can go to OpenSea and search for any NFT or list theirs for sale in a few simple clicks. As NFTs cross the chasm of early adopters and branch out into new applications - OS will find it extremely hard to service all the different use cases.

With over 230,000 distinct NFT collections catering to unique tastes, marketplaces have carved niches in areas such as Gaming (Fractal, Axie Infinity), Digital Fashion (Digitalax), Art ( SuperRare), Sports (Sorare), Music (Royal), Community(Zora).

Revenue Streams

Marketplaces in this segment monetize through a fee for facilitating transactions varying from free to 2.5%. Minting on Zora is essentially free except for gas fees and a tiny charge of $1 per mint which has netted them in excess of $2.5 Mn.

https://twitter.com/pandajackson42/status/1642905741546627074

Building Moats

These markets typically don’t have any moats as users can buy the same NFT across a number of platforms. Marketplaces try to double down on the niche that they are serving and build differentiated product experiences- Zora, for example, makes it really simple to run marketing campaigns and build a community through specialized mint pages. MagicEden integrates games seamlessly, allowing users to play directly on their site without navigating away.

Aggregators: The Middlemen of the Market

Web2 aggregators acquire supply and demand to control the user relationship directly - Netflix acquires content so that users are forced to sign up to their platform to watch content, Uber dangles incentives for taxi drivers and locks them in long-term contracts so that they cannot leave to a competitor. With decreasing costs of transactions, aggregators manage to control so much demand that not being on these aggregators leaves producers unusable- if your page is not on Google, you don’t exist, so you will optimize to be crawled.

In the web3 space, however, the open nature of NFTs discourages ‘lock-in’. NFT aggregators such as Gem and Genie display a variety of NFTs from different sources in a single location. This is similar to how a news aggregator would gather news from various sources or pricing comparison websites check prices across different e-commerce platforms to give the best rates. They interact with other NFT platforms through APIs and pull bids into a consolidated display ‘aggregating’ all liquidity.

NFT buyers and sellers are typically looking for

- Best prices

- Instant transactions

- Wide range of choices

By tapping into the full spectrum of bids, aggregators promise quicker transactions at better rates, luring users. Yet, they cannot monopolize this liquidity; users can easily take their NFTs elsewhere.

One way to control supply is through NFT Automated Market Makers (AMMs). An NFT AMM is a decentralized exchange that allows traders to instantly buy or sell their NFTs through automated liquidity pools. Liquidity providers deposit NFTs and ETH into a pool and set a bonding curve that automatically prices buys and sells, earning a cut of the fees for every trade. NFT AMMs like Sudoswap and Tensor lock NFTs up into pools and if users want to purchase a specific NFT from this pool, they are forced to come to the AMM and buy.

NFT aggregators pull in NFT bids from AMMs as well, offering a consolidated view of all active bids. Take the following interface from Gem where bids are pooled from sources like Sudoswap, and when a user selects a particular NFT for purchase, the transaction is routed to the respective marketplace to finalize the sale.

Revenue Streams

Aggregators usually charge a substantial fee depending on how much control they have over the market - Apple and Android Play stores take 30% of every transaction processed. Youtube takes 30% of creators’ earnings, food delivery aggregators charge 30% of every order delivered.

NFT aggregators navigate a fine balance with low or no fees. Sudoswap charges 0.5% for every transaction from its NFT pools, while aggregators like Gem and Genie currently forgo fees to stay competitive and gain adoption.

Aggregators instead, aim for the ancillary services that complement digital assets. there’s a variety of financial products that can be layered over the core products. After successfully establishing a core user base and addressing their fundamental product needs, aggregators can provide additional financial services at zero distribution cost, reaping significant profit margins. Blur's lending product - Blend is a prime example of this trend, facilitating peer-to-peer loans.

Building Moats

NFT AMMs try to capitalize on liquidity as a moat - once LPs anchor their NFTs on Sudo, they’re typically restricted from listing elsewhere. However, NFT AMMs have a big disadvantage - Due to NFTs' volatile nature and the rigidness of bonding curves, LPs need to constantly manage their positions.

Blur, on the other hand, has devised a unique approach with its liquidity pool, which, standing at $120 million and combined with predetermined bids, enables Blur to manage large-scale transactions efficiently. A distinctive edge for Blur is that these bids are exclusive to their platform and aren't available for sharing with other platforms via APIs. While Blur currently manages bids tied to anticipated rewards, the strategy's sustainability once these rewards wane, is an open discussion.

Infrastructures: The Foundational Players

In the world of Web3, infrastructure evolves into ‘protocols’. These are sets of rules or procedures designed for data exchange. In the same way that the internet uses protocols like HTTP for web browsing, FTP for file transfers, and TCP/IP for data communication, Web3 protocols serve as the ‘rules of the road’ in the Web3 space. These protocols are open, community-owned, and permissionless, meaning they can be freely used by anyone without a requirement for a license.

Opensea's Seaport protocol—which launched last year—is a marketplace contract for creating and fulfilling NFT orders efficiently and safely. The protocol supports many types of orders- instant buy, bulk purchase, and individual sales. The core smart contract is open source and inherently decentralized, with no contract owner, upgradeability, or other special privileges.

- Shared Protocol: Anyone can use Seaport to create a marketplace

- Build Together: Open-sourced with contributions encouraged through PRs

- No protocol fees: Public good that acts as a backbone

- Opt-in upgrades: Nonupgradeability so that neither Opensea nor potential hackers can alter the rules or compromise the contract to steal users'

Users transacting through Seaport only need to pay Eth gas. Think of OS as a frontend that uses the Seaport protocol and charges additional fees(0.5%) for using its frontend. Other marketplaces can also move to Seaport for its efficiency and add their own fees on top of it. Over 1.4Mn users have transacted on Seaport earning over $75M in revenue.

While Seaport is the protocol for exchanging assets, other teams are building protocols for different use cases - Double is building the rental protocol for NFTs, NiftyApes is building the BNPL protocol, Paraspace and Sharky are building lending protocols for NFTs. These protocols enable holders to connect with each other and exchange value.

Tegro is building CLOB infrastructure for NFT trading. They aggregate liquidity across all markets for every collection and support advanced trading features such as limit orders, order books, and bulk trading. Other marketplaces can use Tegro’s protocol to hook into liquidity across all chains.

Protocols bring information on-chain so that anyone can freely build on them, while aggregators and niche marketplaces restrict this information through off-chain order books and give APIs for others to hook into.

Revenue Streams

Web3 protocols are often expected to be public goods and introducing fees at the protocol level can be controversial.

A case in point is Metaplex, the team that’s building “The NFT protocol that underpins the Solana ecosystem”. After raising $46 million for the development of essential tools, including auction protocols, minting toolkit, and Android & iOS SDKs, Metaplex announced that they are transitioning into an NFT infrastructure standard for Solana. This transition included the introduction of a fee of 0.01 SOL per NFT created.

The decision stirred considerable resistance from the community. Many NFT marketplaces, exchanges, and wallets, having constructed their platforms using Metaplex's standards and viewing them as 'public goods,' found themselves confronted with what they perceived as a 'tax' for utilizing Metaplex.

The Metaplex team's responded that maintaining and improving their code demands resources, necessitating a revenue model. This nuanced situation is not isolated to Metaplex. Uniswap’s protocol has a latent fee mechanism that could charge up to 0.05% per transaction if activated.

As Web3 platforms continue to grow and mature, we’ll see more experimentation with revenue streams at the infrastructure level. Some may opt for utility fees, while others could offer added services on top of the core protocols. A comparison can be drawn with open-source ventures like MongoDB and Linux, which provide free software but charge fees for deployment, integration, hosting, and other support services.

Building Moats

The race is towards universal standardization. Once a protocol achieves this gold standard and all transactions happen over this standard, it's a strategic positioning that enables a protocol to anchor itself firmly within the ecosystem. It also fortifies the brand's reputation for security and innovation, creating opportunities for value-added services.

Future Trends

OpenSea is playing the ecosystem game with different offerings across the three layers-with its marketplace in the Long Tail layer to OpenSea Pro in the Aggregator layer, and Seaport in the Infra layer.

OS recognizes that Seaport grants an advantage to competitors such as Blur, who can leverage its liquidity. Despite this, OS is determined to position Seaport as the underlying protocol for all digital exchanges. By presenting its infra layer as a protocol, OS is actively encouraging developers to create new markets, products, and experiences. The team can observe what other utilities devs need and offer them as revenue-generating features.

Other marketplaces are also pushing downwards in the platform stack. Magic Eden started as a Solana marketplace but is transitioning to an aggregator layer by partnering with other aggregators to facilitate multi-market listings and purchases.

The NFT value chain's evolution is propelled by two forces: personalization from “above” and componentization from “below”. This dynamic manifests through several emerging trends:

1. Fragmentation Through Personalization: Niche-specific marketplaces, each finely tuned to cater to distinct tastes and communities will create tailored and immersive experiences putting NFTs at the centre. Picture a sports fan rewatching legendary game moments, collecting autographed memorabilia, or even engaging in virtual meet-and-greets with their favorite athletes. Opensea’s Deals is a p2p swapping protocol that uses Seaport to enable trustless NFT exchange with any stranger.

2. Scalability and Cost Efficiency: Scale will be the defining feature of underlying infrastructure. Who would want to shell out $1000 in gas fees for a weapon skin worth $10? Future protocols will operate across low-cost blockchains, keeping fees minimal and supporting personalized apps like curation, specific listings, and gaming launchpads.

3. The Rise of SaaS Models in Aggregation: Much like IT integration consultants in the traditional tech world that help enterprises hook into Salesforce/Hubspot, the NFT world will see the development of specialized SaaS-based services. Tracking tools like Flip could provide advisory, recommendations, and consulting services to aid in the digital transformation of assets into NFTs.

4. Evolved Store Management: Specialized marketplaces with tools for converting content into NFTs, cataloging, releasing content, fostering artists, and running media campaigns will emerge. These platforms will not only be transaction hubs but also creative laboratories, nurturing artistic innovation and engagement - letting artists build and collaborate on this content. Opepen is an attention machine and a launchpad for artists to create the next set of Opepen NFTs. Instead of releasing art into the void, new artists can get access to Opepen’s community driving their own popularity and success.

5. Rise of Market Makers: The ‘protocolization’ of infrastructure will enable market makers to establish a liquid market for NFTs. Rather than being confined to providing liquidity in a single marketplace, they can run different strategies across platforms.

The NFT landscape is on the brink of a new evolution: digital assets are seeping into technology, art, community, and business. The ongoing tug-of-war between aggregators and infrastructure will continue - aggregators want to control the market, while infrastructures want to champion innovation over their protocols.

If you are building something in this space, don’t forget to hit us up. We would love to shape this evolution together!

Big thanks to Ashish Rawat for his feedback on this piece. Disclosure - We have invested in many of the NFT projects listed here including Magic Eden, X2Y2, NiftyApes, and TegroFi.